Dr. Andrew Griffith

Assistant Professor

Department of Agricultural and Resource Economics

P: 865-974-7480

Many cattle producers are in the midst of marketing the spring born calf crop or are making plans to haul cattle to town. At the same time, those same producers are wondering what their calves will bring from a price standpoint, and they will not know until they are actually sold. This is the make and break point of the year for many cow-calf producers as they find out what their past year of labor was worth in the cattle business.

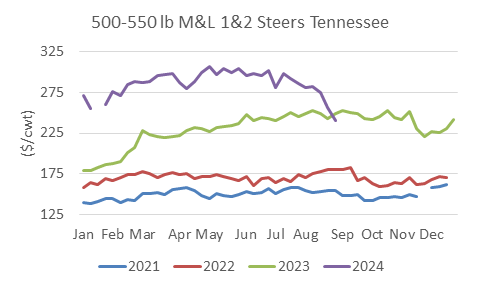

The accompanying figure has the past four years of prices for 500-550 pound medium and large frame, number 1 and 2 muscled steers in Tennessee. The first seven months of 2024 were certainly something to brag about compared to the previous three years, but as the market was heading into September, the price of calves was on a steep decline. All three of the previous years represented in this figure demonstrate softer prices in the fall months at some point, but none of them have any decline to the magnitude of what is seen from the beginning of July 2024 through the end of August 2024 in this figure. This is where the question comes in as it relates to a decline in prices this fall.

Will prices decline further this fall as the large runs of calves come to market, or will the price reverse and gain strength? At the time of this writing, there is no reason to believe prices will turn on a dime and head to lofty peaks. This is especially true given the drought conditions that have become increasingly widespread. This may mean demand locally and across state lines may not be as robust as it is typically. It is difficult to get excited about purchasing relatively high-priced cattle when there is little forage base and profitability is becoming more difficult.

Maybe the most troubling part of all the discussion is that prices in the last quarter of 2024 could be lower than the last quarter of 2023. Given that prices ended August 2024 lower than where they were in August 2023, there is a good chance prices will continue to languish below year ago levels. This is sure to upset many producers who were fully expecting to market cattle on a much stronger market this year compared to last year.

This is where expectations and guarantees are like rubber meeting the road. This is a great example of when Livestock Risk Protection insurance would have been a great investment. Some reading this will say hindsight is 20-20, and making the decision in hindsight is easy. The alternative way of thinking is for producers to consider price risk management as a cost of production and purchase an insurance product when prices being offered at a future date are beneficial to the operation.

Again, there are still others who will disagree with this statement, because they feel a person can sell overvalued animals and purchase undervalued animals at all times in a year. This is not incorrect, but many cow-calf producers have no desire to operate in this manner. Thus, one has to determine how to manage for profits within their given parameters of production.

In order to move past this discussion, the conversation can revert back to price expectations this fall. It is going to be difficult for calf prices to rebound this fall due to several factors. Some of which have been discussed while others have been omitted for brevity. There is no reason to believe cattle prices will revert back to levels in 2021 or 2022, but it is also difficult to provide support for prices moving back to levels witnessed the first half of 2024 as the market moves to 2025. The fundamentals of the market support strong cattle prices, but economic uncertainties have outweighed the fundamentals at this time.